AUDIT 101: SAIs’ mission, structure, mandate, and various models

Linking SAIs work to the broader PFM cycle

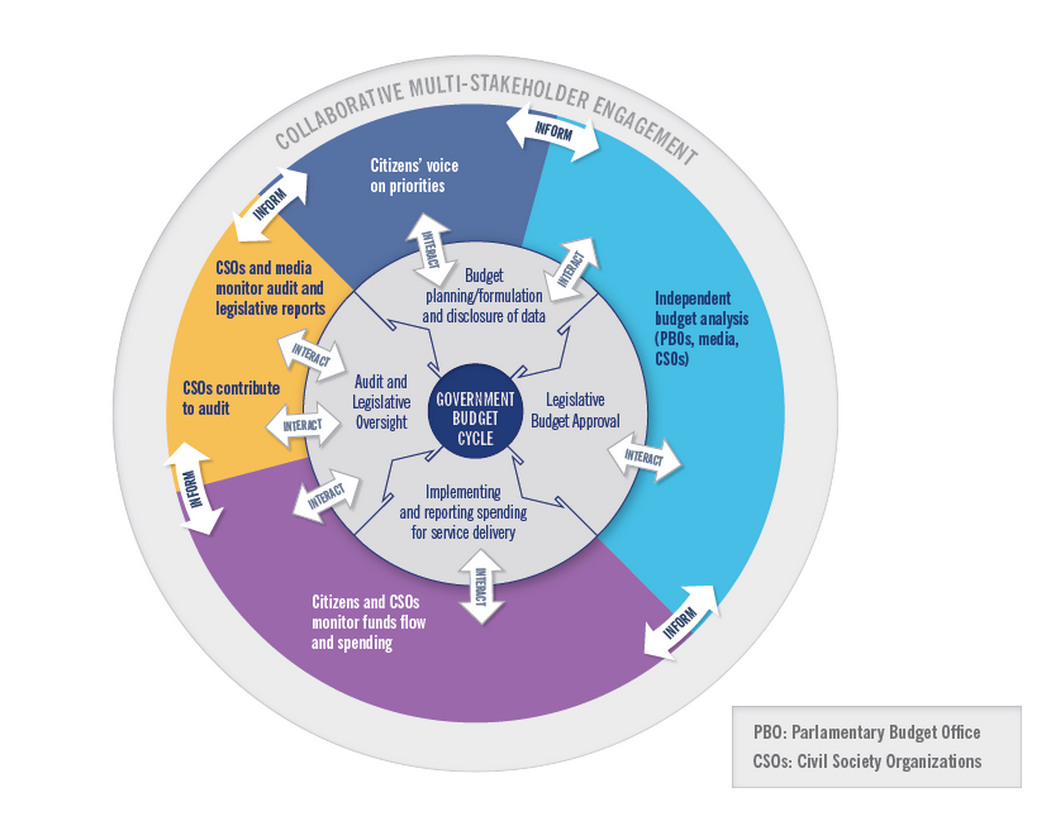

Public financial management (PFM) provides a good framework to place citizen engagement with SAIs in context. As a central element in governance reforms, PFM focuses on the technical aspects of budget implementation and procurement execution, or on the governance aspects of the planning, budgeting, and audit stages. That focus is important because having an effective, efficient, and transparent financial management system in place is instrumental in achieving national development goals and outcomes. With that in mind, SAI–CSO engagement contributes to better audit and oversight of the use of public money in procurement. Moreover, as the quality of their engagement deepens, CSOs—through their partnership with SAIs—can provide grounded insights on the quality and responsiveness of government programs, which, when used properly, can strengthen the overall PFM cycle. That relationship is best illustrated in figure 1: Collaborative multi-stakeholder engagement in the PFM cycle.

Additional resources can be found through the following links:

Introduction to PFM PFM Planning Stage PFM Budgeting Stage PFM Expenditure Management Stage PFM Procurement Stage PFM Performance Assessment Stage