AUDIT 101: SAIs’ mission, structure, mandate, and various models

SAIs´ models and characteristics

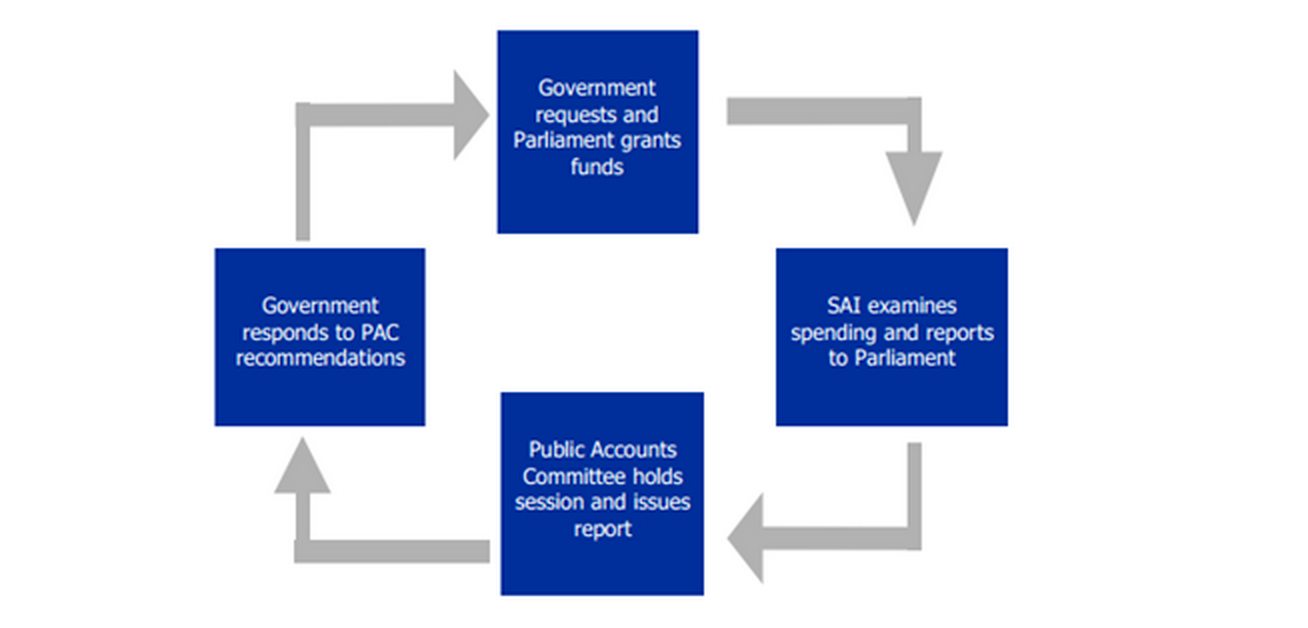

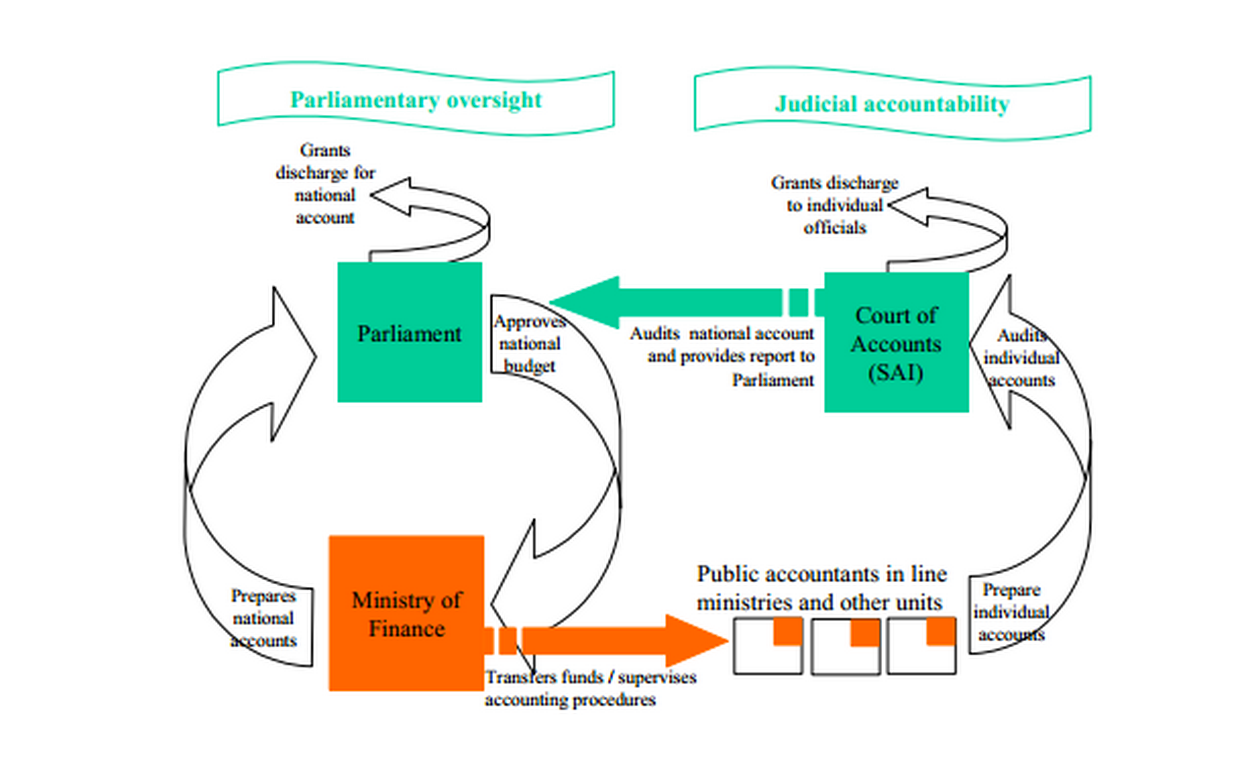

SAIs may fall into one of three broad organizational categories, depending on the institutional set-up and accountability system within a given country context: the Westminster model; the Board, or Collegiate model; and the Court, or Judicial model (also called the Napoleonic model). Each model displays distinctive features in the scope of audit tasks, the SAI´s enforcement authority, and its relationships with the legislature. Table 1 lists the main characteristics of each SAI model.

|

SAI Model |

Westminster |

Board/Collegiate |

Court/Judicial |

|

Head |

Auditor General (AG) or Comptroller General (CG) |

President |

President/First President |

|

Organizational structure |

Monocratic General Audit Office or Comptrollers´ General

|

Collegiate

|

Collegiate Court of Auditors or Tribunals of Accounts

|

|

Accountability system |

Parliamentary

|

Parliamentary

|

Judicial

|

|

Relations with parliament |

|

|

|

|

Types of audit |

|

|

|

|

Reporting |

|

|

|

|

Strengths |

|

|

|

|

Weaknesses |

|

|

|

|

Examples |

|

|

|

Source: DFID 2004.

Source: DFID 2004.